This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

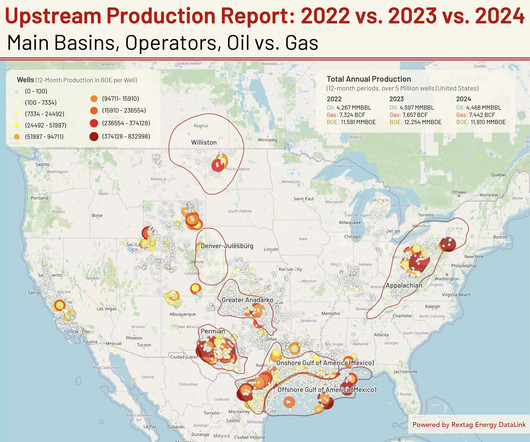

This report analyzes upstream oil and gas production trends over the last three years, based on data from Rextag Energy DataLink. MMBBL 193 BCF Analysis: Hilcorp leads in gas production but is less significant in oil output. MMBBL 193 BCF Analysis: Hilcorp leads in gas production but is less significant in oil output.

(World Oil) – Libyas oil and gas sector is set for a new era of growth and investment following the announcement of its first exploration bid round in 17 years. Momentum is already building across Libyas energy industry, with several upstream developments demonstrating the countrys renewed focus growth and investment.

(World Oil) – Africas national oil companies (NOC) are moving beyond operating as state-representatives by transforming themselves into competitive upstream players. These efforts reflect a broader trend across the continent, where NOCs are leaning on foreign partnerships to advance oil and gas production.

Upstream Midstream Downstream are terms commonly used in the oil and gas industry to describe different stages of the production and distribution process. Each sector has distinct activities and focuses on specific aspects of the overall oil and gas supply chain. What is oil and gasupstream midstream downstream?

Todays TRADITIONAL SUPER BASINS of oil & gas will not meet the challenges of sustainability and achieving Net-Zero by 2050. For the upstream industry to become more sustainable, it must focus on resources that are co-located with both plentiful clean electricity and CCS potential.

upstream M&A reaching $105 billion in 2024the third highest as recorded by Enverusthe market shows no signs of slowing down, with high price tag deals being driven by the scarcity of high-quality inventory. Diamondback is one of the largest players in the Permian Basin, second only to Exxon Mobil, based on gross operated oil volumes. [1]

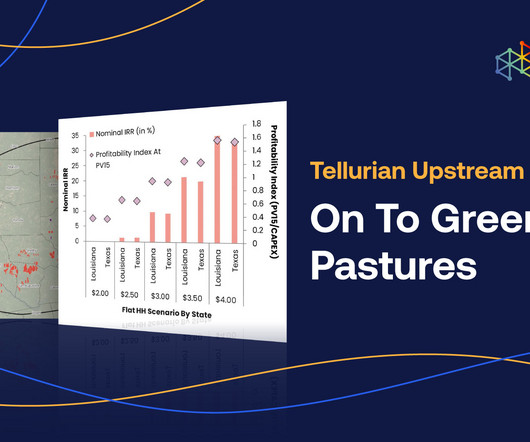

Aethon has agreed to purchase Tellurians upstream assets for (US) $260MM below street estimates, which ranged from $270MM to $500MM. Below, we reflect on the deal and walk through what might be next for the play now that gas prices are back in the mid $2/Mcf range. Basin-wide, however, ~$3.00/Mcf Source: Novi Insight Engine.

This years Unconventional Resources Technology Conference (URTeC) was a whirlwind for the Novi team, filled with insightful talks, technical discussions, and exciting new developments in the oil and gas industry. The basin has ~9 years of remaining inventory that can generate a two-year payout period at current WTI prices.

Rystad forecasts QatarEnergy will invest between US$14-15bn per year over the next few years as it continues to invest heavily in the North Field gas field and expanding LNG capacity, while ADNOCs expenditure, which reached US$5.7bn last year, is forecast to increase given its target of 5mn bpd production capacity by 2027.

Resource optimization is the key challenge facing oil and gas companies today. During exploration and other upstream activities, optimizing resources depends on accurate models that illuminate the subsurface potential. Want to learn more about IBM solutions for Oil and Gas?

Earnings per share plummeted to $2.25, and the decline was largely due to a 14% dip in crude realisations and a spine-tingling 60% decrease in natural gas realisations. Despite this trick rather than treat, ExxonMobil boosted production by 80,000 oil-equivalent barrels daily, driven by growth in the Permian Basin and Guyana.

The Permian Basin continues to see significant shifts in ownership as oil and gas operators refine their asset portfolios. Understanding Air Permits in Oil & Gas Transfers When ownership of an oil and gas facility changes, the new operator must update regulatory permits to reflect the transition.

oil and gas industry is experiencing one of its most transformative periods. Now, as we step into 2025 , the industry faces critical questions : Which basins will see the most growth? oil & gasbasins , the leading companies , and market trends using the latest data and forecasts. Natural Gas Production: 25.8

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content